Share

How to Use Blockchain in Business – A Complete Guide

- BLOG

- Uncategorized

- March 27, 2025

Most businesses are drowning in slow approvals, clunky paperwork, and processes that barely talk to each other. If that sounds familiar, you’re not alone. It’s exactly where blockchain can make a difference. The companies already using it? They’re gaining speed, trust, and a serious edge.

So, how to use blockchain in business? You’ll need to identify a workflow to improve, select a suitable blockchain platform, develop a proof of concept, and integrate it with your existing systems. Businesses leverage blockchain to automate transactions, enhance transparency, secure data, and eliminate intermediaries.

Want to know which platforms work best, what use cases actually deliver results, and how to use blockchain in business step-by-step? Keep reading.

Contents

- 1 The Core Principles That Make Blockchain Different for Business

- 2 Integrate blockchain in your business systems with Webisoft!

- 3 Types of Blockchains: Choosing the Right Protocols

- 4 How to Use Blockchain in Business: Applications & Technologies

- 5 How to Use Blockchain in Business (A Step-by-Step Guide)

- 5.1 Step 1: Identify the Business Challenges Blockchain Can Solve

- 5.2 Step 2: Choose a Blockchain Platform

- 5.3 Step 3: Integrate Smart Contracts for Automation

- 5.4 Step 4: Address Security and Compliance

- 5.5 Step 5: Pilot and Scale

- 5.6 Step 6: Integrate with Existing Systems

- 5.7 Step 7: Train Your Team and Launch

- 6 Blockchain-as-a-Service (BaaS): How to Use Blockchain in Business in The Easiest Way

- 7 How to Use Blockchain in Business: Connect Everything with Interoperability and Standards

- 8 Challenges and Solutions to Overcome Blockchain Errors

- 9 How Webisoft can Help You Integrate Blockchain in Your Business

- 10 Integrate blockchain in your business systems with Webisoft!

- 11 Conclusion

- 12 FAQs

The Core Principles That Make Blockchain Different for Business

Understanding the core principles of blockchain will simplify the learning process of how to use blockchain in business. The core principles are:

Decentralization

All your departments, partners, and vendors see and use the same shared record. No more “who changed this?” headaches due to the blockchain database’s decentralization. There’s no lone IT admin or siloed database. Everyone you trust gets the same, up-to-date view.

Immutability

Once something’s in, it’s in for good. If your finance team logs a payment or your warehouse marks a delivery, that record is permanent.

Need to fix a mistake? You don’t have to overwrite; simply adding a new entry will do the job. The full story is always there, no cover-ups.

Selective Transparency

You control who sees what. Maybe your logistics partner checks shipment status while your CFO reviews all transactions. Everyone has access to what they need, nothing more. It’s open where it helps, private where it counts.

Integrate blockchain in your business systems with Webisoft!

Schedule a free consultation today and unlock the full value of blockchain for your business.

Types of Blockchains: Choosing the Right Protocols

Choosing the right blockchain architecture isn’t about what’s popular. It’s about what fits your business, your data, and who you’re working with. Here are three types of blockchains:

1. Public vs Private Blockchains

Before you pick between these two types of blockchain, take a look at the differences between them:

| Feature | Public Blockchain | Private Blockchain |

| Access | Anyone can join and participate | Only authorized users can join and validate |

| Transparency | Fully transparent; all transactions are public | Limited to permitted users; data is private |

| Speed | Slower due to many nodes and network congestion | Faster with fewer nodes and less traffic |

| Security | Highly secure, decentralized, hard to tamper with | Secure, but more vulnerable due to central control |

| Governance | Decentralized, community-driven | Centralized or semi-centralized, business-controlled |

| Privacy | Low; all data is visible | High; sensitive data stays confidential |

| Best For | Open apps, public records, tokenization | Enterprise apps, internal processes, compliance |

| Cost Efficiency | Higher costs due to transaction fees | More cost-effective at scale |

| Customization | Limited | Fully customizable to business needs |

While private blockchains are generally more suitable for most business applications, they’re not always the definitive solution.

In enterprise settings, private blockchains offer clear advantages. They allow organizations to —

- Maintain control over participants

- Customize the infrastructure to meet regulatory needs

- Protect sensitive data

This makes them ideal for industries like finance, healthcare, supply chain, and government services.

However, public blockchains have their place, especially when transparency, trustlessness, and openness are essential. For example:

- Tokenized assets, NFTs, and decentralized finance (DeFi) products benefit from public blockchains because users require full visibility and control.

- Public registries, such as land ownership or academic credentials, gain legitimacy from the open, immutable nature of public chains.

2. Hybrid Blockchains

Now, sometimes you want the best of both public and private blockchains. That’s where hybrid blockchains come in.

You might use a private network for internal operations but publish selected data to a public chain for transparency or audit purposes. Use hybrid blockchains when you:

- Need privacy internally but still want to prove authenticity externally

- Bridging legacy systems with public trust mechanisms

- Want to scale transparency gradually

3. Consortium Blockchains

Consortium blockchain is one of the blockchain protocols that’s shared between a group of trusted organizations, like manufacturers, banks, logistics providers, or insurers.

Everyone in the group gets a say, but the network isn’t open to the public. It’s not fully private either; it’s semi-trusted, semi-decentralized.

For example, in a global food supply chain, you might have growers, shippers, retailers, and regulators all running nodes. Each sees relevant data, validates only what they’re involved in, and works off the same ledger.

Use consortium blockchains when you:

- Work across multiple companies or competitors

- No single player should have total control

- Need shared data standards but controlled access

How to Use Blockchain in Business: Applications & Technologies

Here are some blockchain example in real-life use cases and applications to make business operations easier and smoother for you:

1. Automating Agreements and Payments

Smart contracts on blockchain automate business agreements, removing the need for manual approvals and paperwork.

For example, in shipping, a smart contract releases payment automatically when GPS data confirms delivery. This reduces errors, speeds up transactions, and eliminates unnecessary middlemen.

Technologies Used for This Task

- Smart Contracts: Self-executing code that enforces business rules.

- Programmable Blockchains (e.g., Ethereum): Platforms for arranging smart contracts.

- Oracles: Middleware services that securely deliver external data (from sources like IoT or APIs) to smart contracts on the blockchain.

2. Securing Supply Chains

Blockchain technology is perfect for securing the supply chain. Now, what is blockchain in supply chain?

It tracks products from origin to delivery, providing real-time visibility and reducing fraud. Retailers use it to trace food items or verify the authenticity of luxury goods, cutting investigation times and improving recall efficiency.

Technologies Used for This Task

- Distributed Ledger: Shared, tamper-proof record of transactions.

- Private Blockchains (e.g., Hyperledger Fabric): Used for enterprise supply chains.

- IoT Integration: Physical devices like sensors or GPS trackers that generate practical data and feed it directly into the blockchain system.

3. Simplifying Asset Ownership and Investment

Blockchain makes it easy for businesses to create, manage, and transfer ownership of both physical and digital assets.

Nike, for example, issues NFTs as digital proof of ownership for sneakers. Real estate firms tokenize properties so people can buy, sell, or trade fractional shares, making investment more accessible.

Technologies Used for This Task

- NFT Standards (ERC-721, ERC-1155): For creating unique digital assets.

- Tokenization Platforms: Convert assets into blockchain-based tokens.

- Digital Wallets: Store and transfer ownership securely.

- Decentralized Marketplaces: Enable trading of tokenized assets.

4. Improving Compliance and Auditing

Blockchain’s immutable ledger makes business records easy to verify and audit. Companies use it to automate compliance reporting and reduce the risk of errors or fraud. Auditors can instantly verify transactions, saving time and increasing trust.

Technologies Used for This Task

- Immutable Ledger: Makes sure records can’t be changed or deleted.

- Automated Reporting Tools: Pull compliance data directly from the blockchain.

- Access Controls: Restrict who can view or edit sensitive information.

5. Improving Customer Engagement and Loyalty

Businesses use blockchain to build customer loyalty programs that are transparent and easy to manage. Loyalty points can be issued as tokens, tracked in real time, and redeemed across multiple brands or platforms.

Technologies Used for This Task

- Tokenization: Turns loyalty points into digital tokens.

- Smart Contracts: Automate rewards and redemptions.

- APIs: Integrate blockchain loyalty programs with existing business systems.

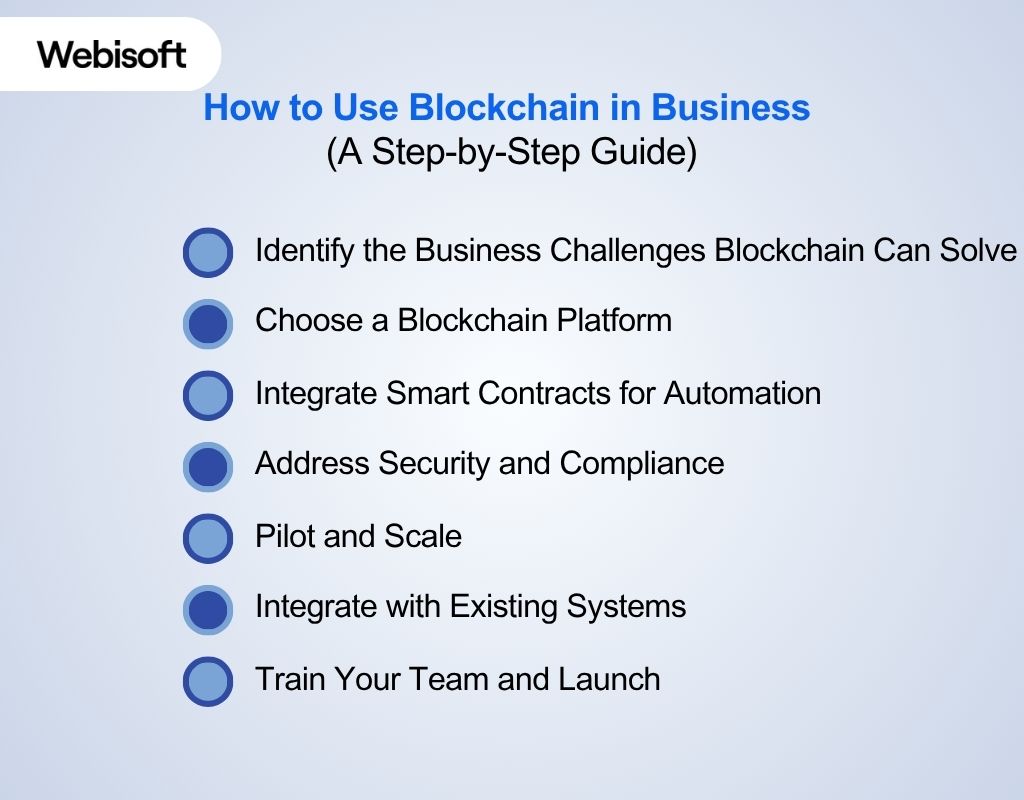

How to Use Blockchain in Business (A Step-by-Step Guide)

Whether you’re looking to automate transactions, improve supply chain visibility, or protect customer data, blockchain can do it all. Here are some how to use blockchain in business examples:

Step 1: Identify the Business Challenges Blockchain Can Solve

First things first, you need to figure out what problems you’re trying to solve. Are you facing data security risks, high costs from intermediaries, or slow payment and contract processes?

Blockchain is best used for issues like tracking products in your supply chain or automating transactions. Define exactly what you want to improve before moving forward.

Step 2: Choose a Blockchain Platform

Once you’ve identified your business problem, picking the right blockchain platform is crucial. Here are the top options and why you might choose each:

- Ethereum

Use Ethereum if you want an open, public blockchain where anyone can join. It’s known for smart contracts, token creation, and building decentralized apps that anyone can access.

- Hyperledger Fabric

Choose Hyperledger Fabric when you need a private, customizable network for your business.

It’s built for organizations that want to control who joins, set detailed permissions, and keep data private between partners. Best for complex supply chains or multi-company collaborations.

- IBM Blockchain

IBM Blockchain is a managed service based on Hyperledger Fabric, but it’s all about ease and support.

IBM handles setup, security, and integration with your existing systems, so you get Fabric’s features without having to build or maintain the network yourself.

- Corda

Go with Corda if you’re in a heavily regulated industry like banking or insurance.

Corda focuses on confidential, direct transactions between parties and is designed to meet strict compliance standards. It’s built for businesses where privacy and legal clarity are non-negotiable.

- Quorum

Pick Quorum if you need the power of Ethereum but with enterprise-grade privacy and performance.

It’s ideal for financial applications that require faster transactions, private smart contracts, and permissioned access, perfect for banks and institutions needing more control.

- MultiChain

Use MultiChain when you want to create a private blockchain quickly and easily. It’s designed for businesses that want secure, permissioned blockchain infrastructure for internal recordkeeping, asset tracking, or audit logs.

- OpenChain

Choose OpenChain if your focus is on digital asset issuance and control. It’s a simpler, scalable platform designed for organizations managing things like loyalty points, vouchers, or company credits. OpenChain provides full control over transactions and access without mining processes.

- Stellar

Go with Stellar if your business involves cross-border payments or digital currencies.

Stellar is built for speed and low transaction costs, making it perfect for remittances, tokenized fiat, or creating accessible financial tools in emerging markets.

Step 3: Integrate Smart Contracts for Automation

Smart contracts are not just software; they’re immutable, self-executing programs stored directly on the blockchain. Once established, they run exactly as coded and can’t be altered, ensuring full trust and transparency across business operations.

These contracts are powered by the blockchain’s virtual machine, enabling automatic actions, like triggering payments or updating records.

For businesses, this means less manual approval, no middlemen, and fewer delays. Whether you’re managing supply chains, processing invoices, or onboarding partners, smart contracts bring consistency, security, and speed.

Step 4: Address Security and Compliance

You can’t afford to overlook data protection or legal requirements. Build these into your project from the start.

- Use a permissioned blockchain for sensitive business data.

- Encrypt all confidential information, both on-chain and off-chain.

- Set up role-based access controls so users only see what they need.

- Schedule regular security and compliance audits.

- Make sure your design meets all relevant regulations (like GDPR or SOX).

Step 5: Pilot and Scale

A pilot involves establishing a small, controlled version of your blockchain solution in a real business environment.

It evaluates performance, ease of use, and overall impact before a full rollout. Here’s how to run the pilot and scale for your business:

1. Build and Launch a Focused Pilot

Start small. Pick one focused use case, like automating contract approvals or tracking product shipments.

- Assemble a cross-functional team from IT, ops, compliance, and any departments affected by the pilot.

- Define what success looks like: faster processing, fewer errors, or better transparency.

- Build a POC that mimics the real workflow, using live data but isolated from your core systems. It’s necessary because it shows whether blockchain can actually solve your problem.

- Run it in a controlled environment with real users. Observe how they interact with it, like what clicks and what confuses them.

- Collect feedback on performance, usability, integration issues, and overall impact.

2. Analyze Results and Refine

Don’t expect perfection on the first try.

- Review metrics, such as transaction speed, error rate, user adoption, and integration stability.

- Document what worked and what didn’t.

- Fix the gaps. Maybe the contract logic needs refining. Maybe users need more training. That’s normal.

- Check compliance and security. If it’s handling sensitive data, make sure it meets all internal and legal standards.

3. Present to Stakeholders

You need to confirm the result and make sure it fits well with your business operation.

- Summarize results for decision-makers. Are the metrics strong enough to move forward?

- Share key learnings, team feedback, and a simple roadmap for expansion.

- If it’s a yes, move on with scaling.

4. Prepare to Scale

Here’s how you should prepare for scaling:

- Check your infrastructure. Can your blockchain setup handle more users, more transactions, and more integrations?

- Set governance rules. Who controls what? Who can approve, audit, or change smart contracts?

- Build an onboarding plan. Make it easy for new users to join, like credentials, training, FAQs, and support.

- Plan your rollout timeline and budget. Know who’s doing what, when, and with what resources.

A pilot involves establishing a small, controlled version of your blockchain solution in a real business environment.

It evaluates performance, ease of use, and overall impact before a full rollout. Here’s how to run the pilot and scale for your business:

Step 6: Integrate with Existing Systems

Once you are ready with all the necessary data and decisions, it’s time to put your data and blockchain into use. But how to use blockchain in business?

For blockchain to make a real difference, it needs to connect smoothly with your current business tools and processes. Here’s how to do it:

- Map Your Systems: List all the software and platforms you use, like ERP, CRM, inventory, payments, and more.

- Identify Integration Points: Decide where blockchain will add value, such as tracking shipments, automating payments, or recording transactions.

- Develop or Use APIs: Use existing APIs or build new ones to connect your legacy systems with the blockchain platform.

- Standardize Data Formats: Make sure data is labeled and formatted consistently so information flows correctly between systems.

- Test End-to-End: Simulate real transactions to confirm everything works seamlessly from start to finish.

- Monitor and Optimize: Track performance and fix any issues as they come up to keep operations running smoothly.

Step 7: Train Your Team and Launch

A successful launch depends on people, not just technology. Make sure everyone is ready. Here’s how you can train your team:

- Develop clear training materials, such as videos, guides, and FAQs.

- Hold hands-on workshops so users can practice in a safe setting.

- Assign “blockchain champions” in each department to support their teams.

- Launch in phases, starting small and expanding as confidence grows.

- Track adoption and performance, and keep optimizing as you go.

Blockchain-as-a-Service (BaaS): How to Use Blockchain in Business in The Easiest Way

Most businesses don’t prefer building custom infrastructure for blockchain. That’s when you can rely on Webisoft for Blockchain-as-a-Service (BaaS) besides their full blockchain development service.

It’s like cloud hosting, but for blockchain. You pick a platform, click a few buttons, and you’ve got a working blockchain network.

Big companies like Microsoft Azure, IBM, and AWS offer managed blockchain platforms. Through this service, you get smart contract tools, secure networks, and integrations without having to build anything from scratch.

When Should You Use BaaS

Pick BaaS when you want to test or deploy blockchain quickly without managing complex infrastructure. It’s ideal if you’re exploring blockchain for the first time or need a fast, low-risk way to prove value.

Webisoft handles it all for you. From choosing the right BaaS provider to setting up the network, integrating your systems, and deploying smart contracts, they take care of the tech so you can focus on your business.

How to Use Blockchain in Business: Connect Everything with Interoperability and Standards

Using blockchain in business is about making sure it plays well with everything else you already use. That’s where interoperability and standards come in.

Your blockchain solution needs to speak the same language as your existing systems, like ERP, CRMs, and databases. That means aligning your blockchain setup with:

- Common data formats and APIs to integrate blockchain smoothly with your existing systems

- GS1 standards for consistent product and supply chain tracking

- ISO standards to meet global security and data integrity requirements

- W3C standards for compatibility with modern web applications and services

Also, if your business interacts with more than one blockchain (like Ethereum and Hyperledger), you’ll need blockchain bridges or middleware.

Challenges and Solutions to Overcome Blockchain Errors

There are a few hurdles of blockchain you’ll face when implementing it in your business. None of these are deal-breakers, but knowing about them ahead of time makes things a lot smoother.

- Scalability: Can Blockchain Keep Up?

Blockchain must scale as your business grows. Early platforms like Ethereum faced congestion (e.g., CryptoKitties). Modern fixes like Layer-2 protocols and sharding increase capacity. Choose the right platform and plan early.

- Regulatory Uncertainty: Navigating the Rules

Regulations around blockchain and crypto change quickly, and what’s compliant today might not be tomorrow.

If your business handles crypto payments or sensitive data, you’ll need to monitor legal updates, document everything, and work closely with advisors who understand both tech and law to avoid costly compliance mistakes.

- High Initial Costs: Is It Worth the Investment?

Blockchain setup isn’t cheap. You’ll face upfront costs for development, talent, and infrastructure. But, like solar panels, the payoff comes over time.

If your business runs high-volume, repeatable processes, blockchain’s efficiency and error reduction can deliver real ROI. For smaller operations, waiting might make more sense.

How Webisoft can Help You Integrate Blockchain in Your Business

How can businesses use blockchain? You need a professional who will integrate it into your business. Webisoft is a leading blockchain development and consulting firm that helps businesses of all sizes harness blockchain technology for real results. Here’s how:

Custom Blockchain Solutions

Webisoft builds secure and custom blockchain platforms that fit your unique business requirements, whether you need a private supply chain ledger, a DeFi platform, or a secure NFT marketplace.

Smart Contract Development

Their team designs, audits, and deploys secure smart contracts to automate business logic, agreements, and transactions, removing manual steps and reducing errors.

Seamless System Integration

Webisoft connects blockchain to your existing ERP, CRM, or payment systems using custom APIs and middleware, ensuring smooth data flow and minimal disruption.

Security & Compliance

They prioritize security and regulatory compliance with continuous testing, regular audits, and adherence to standards like GDPR, SOC 2, and ISO 27001.

Consulting & Strategy

Webisoft’s experts guide you through platform selection (Ethereum, Hyperledger, Corda, and more), use case identification, and long-term blockchain strategy.

End-to-End Support

From initial brainstorming to post-launch support, Webisoft covers every phase, so you can focus on your business while they handle the tech.

Get started with blockchain integration by scheduling a blockchain consultation with Webisoft today. Let their experts show you how blockchain can transform your business.

Integrate blockchain in your business systems with Webisoft!

Schedule a free consultation today and unlock the full value of blockchain for your business.

Conclusion

In conclusion, how to use blockchain in business is a journey that can transform your operations. By improving security, reducing costs, and automating processes, blockchain offers valuable solutions.

Start small by identifying key areas where blockchain can help, then scale as you see success.

If you’re ready to integrate blockchain into your business, contact Webisoft for personalized solutions and expert guidance that will make your transition smooth and impactful.

FAQs

Here are some commonly asked questions regarding how to use blocking in business:

What types of businesses benefit from using blockchain?

Businesses in sectors like finance, supply chain, healthcare, and e-commerce can significantly benefit from blockchain’s transparency, security, and efficiency. It’s ideal for any business needing secure transactions and streamlined operations.

Can blockchain be integrated with existing business systems?

Yes, blockchain can be integrated with existing business systems using API integrations or hybrid solutions. It allows businesses to attach blockchain while maintaining current processes.

How does blockchain affect regulatory compliance?

Blockchain creates immutable records, making it easier for businesses to comply with regulations and pass audits. It ensures transparency and provides verifiable data for reporting.